Average True Range Indicator Calculation

What Is Average True Range Fidelity

Average True Range Atr Chartschool

/ATR-5c535f8fc9e77c000102b6b1.png)

Average True Range Atr Definition

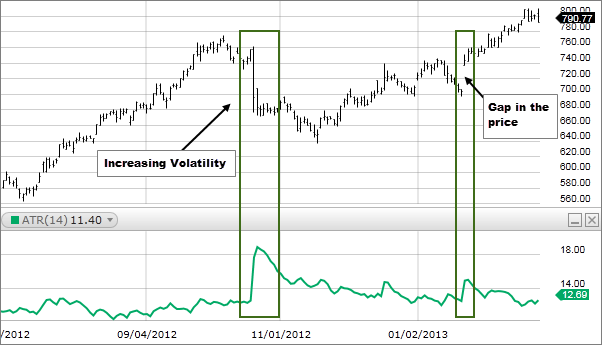

Measure Volatility With Average True Range

How To Use The Atr Indicator The Universal Trading Tool

Incredible Charts Average True Range Atr Trailing Stops

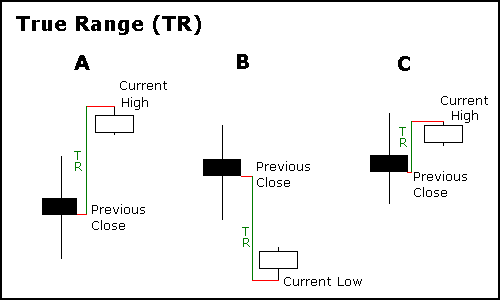

The average true range atr is an exponential moving average of the true range.

Average true range indicator calculation.

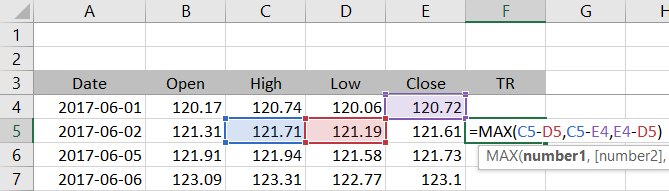

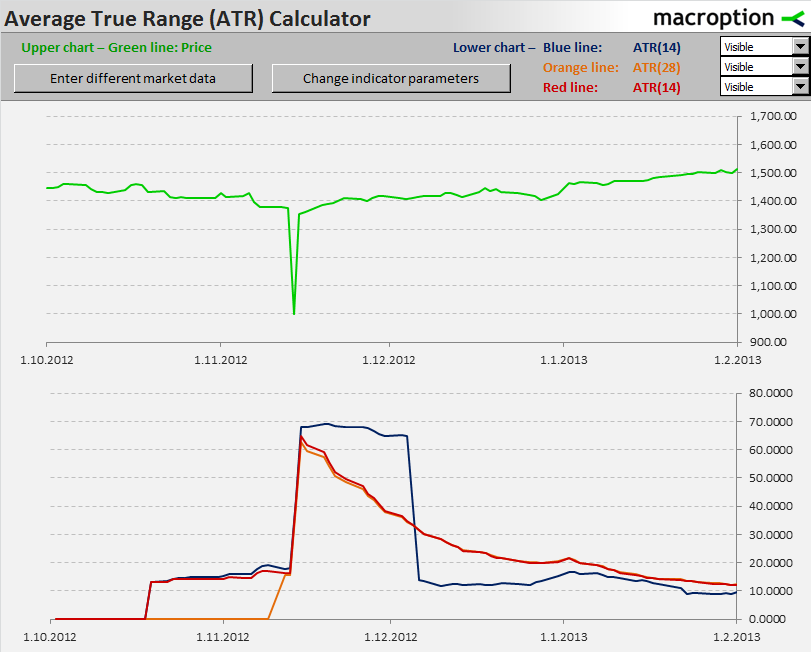

Calculating Average True Range Atr In Excel Macroption

How To Set A Stop Loss Based On Price Volatility Babypips Com

How To Measure Volatility In Forex Babypips Com

3 Ways To Identify A Ranging Market With Your Algo Quant News

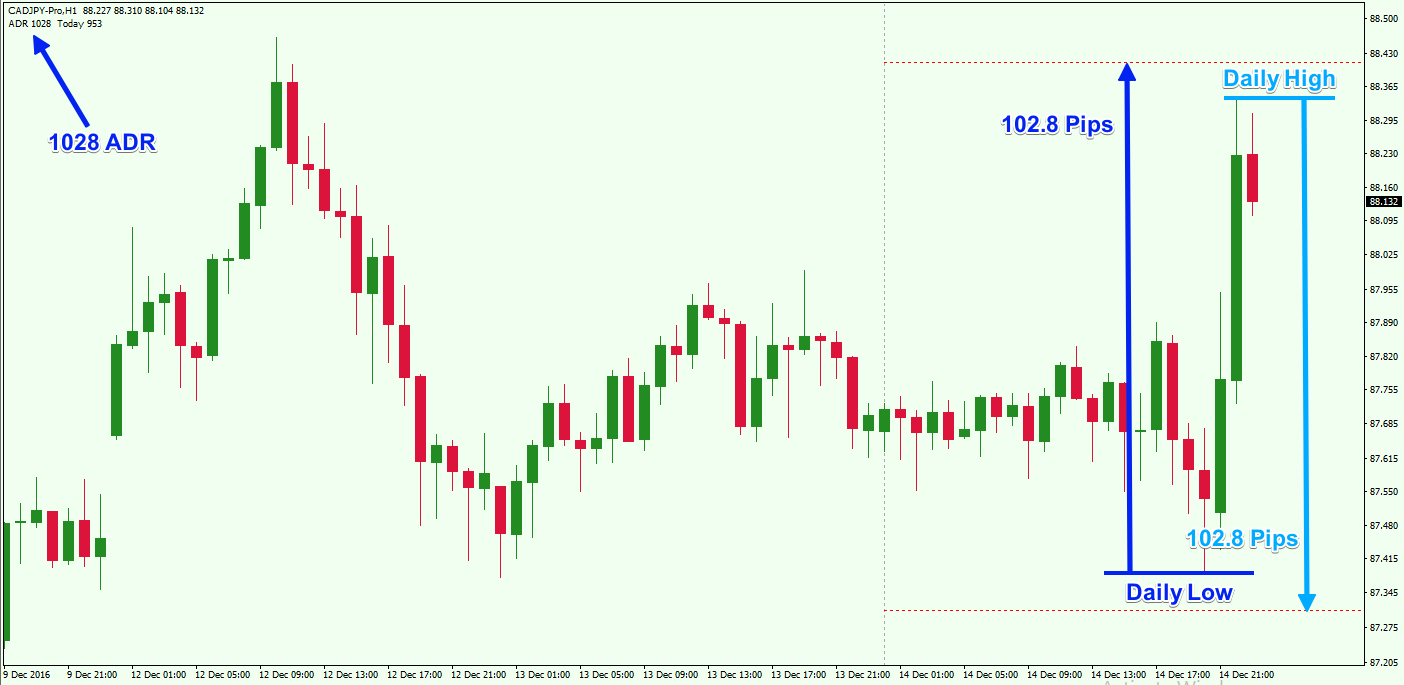

A Unique Way To Use Average Daily Range To Your Advantage

How To Read And Apply The Atr Indicator For Stock Trading

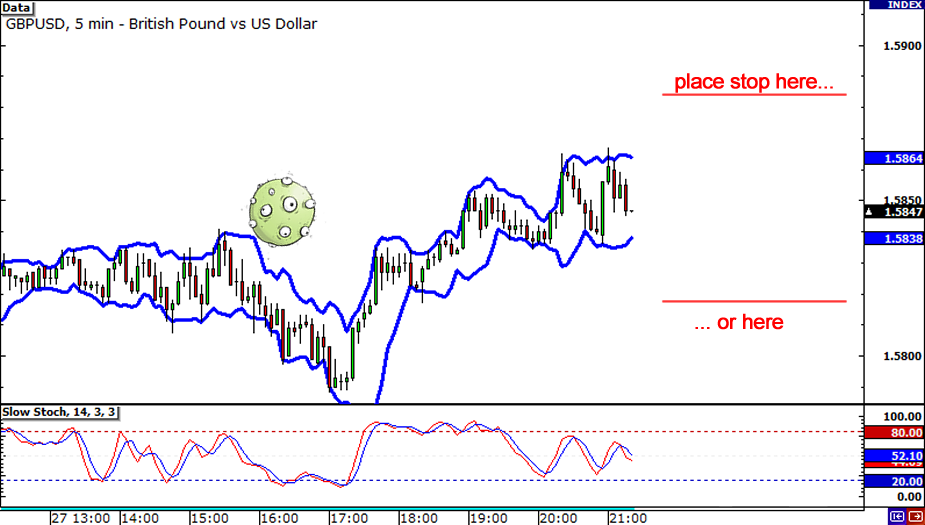

A Logical Method Of Stop Placement

Average True Range Excel Calculation Tutorial 2020

Atr Calculation Methods And Formulas Macroption

What Is The Atr Indicator How Do You Use It When Trading Mt4

Your Ultimate Guide To Trade With Average True Range Atr Indicator Capital Com

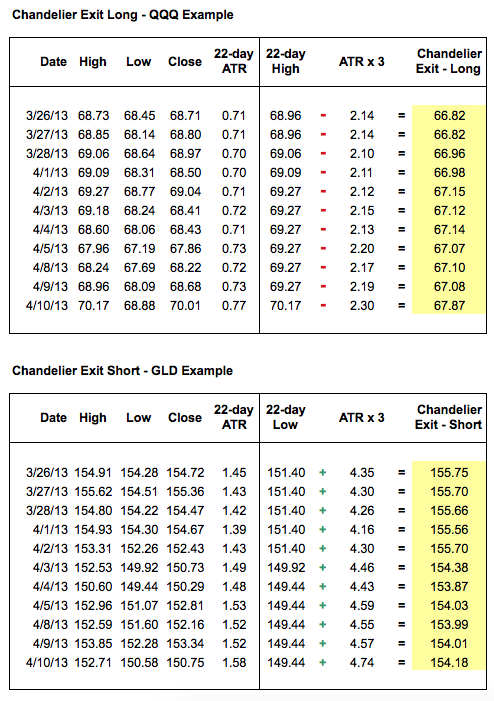

Chandelier Exit Chartschool

How To Calculate Average Daily Range Of A Stock General Trading Q A By Zerodha All Your Queries On Trading And Markets Answered

Average True Range Atr True Trading Strategies Moving Average

Supplementary Notes 1 Varsity By Zerodha

Using Adr Average Daily Range To Find Short Term Trading Opportunities Forex Training Group

Atr Average True Range Technical Indicators Youtube

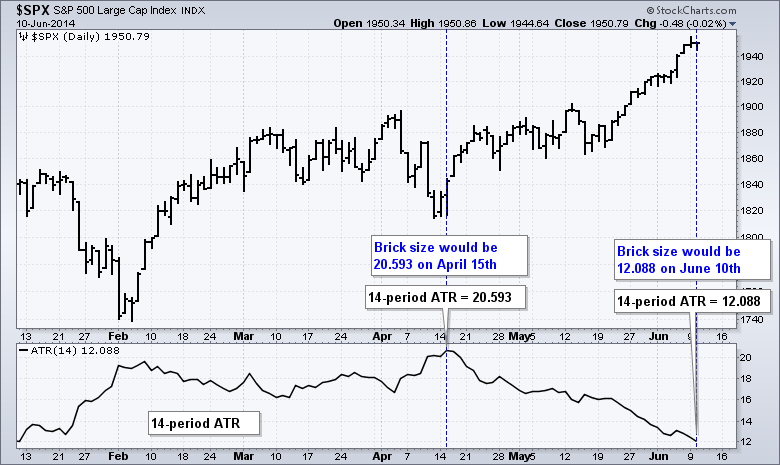

Renko Charts Chartschool

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcstlvvu7 3i3s6 Zef2yypdlizeqaij7ds86gnwo2 Khnfistly Usqp Cau

This Indicator Acts As A Ratchet Stop Loss To Protect Short Positions And Measures The Average True Range Over A Pre Defined Period In Positivity Web Design Responsive Web

Incredible Charts Stochastic Rsi

A Volatility Based Momentum Indicator For Traders By Steve Roehling Medium

Average True Range Indicator Explained Simply In 3 Minutes Youtube

Download Atr Stop Loss System For Amibroker Afl

Source : pinterest.com